Opinion: Poonam Gupta.

In September this year, India will complete 8 years since it implemented Inflation Targeting (IT). Consistent with the experience of other countries, in India too, IT has been credited with improved outcomes: gentler and less volatile headline inflation; anchored inflationary expectations; improved communication and transparency; enhanced transmission of monetary policy; greater independence of the central bank; better coordination with the fiscal authorities; and smooth conduct of exchange rate and reserve management policies in response to external shocks.

The RBI has remained as committed to a ‘multiple indicators’ approach as it was before the formal adoption of IT. A text analysis of its statements shows that the monetary policy committee considers a range of factors before arriving at a decision, such as drivers of inflation, dynamics of food and core inflation, liquidity situation, global economic environment and risk appetite, output gap, capacity utilization, inflationary expectations, exchange rate, employment, and fiscal deficit.

Despite this apparent successful run, there are periodic calls to make changes in the IT framework. One such proposal is that instead of CPI headline which includes demand- induced volatile food prices, core inflation or WPI inflation should be targeted. In the most direct official statement to this effect, the latest Economic Survey has proposed that “India’s inflation targeting framework should consider targeting core inflation, excluding food”.

The arguments in favour are that monetary policy is ineffective in combating supply- driven food inflation; food inflation is higher than the core inflation resulting in tighter monetary policy; and that food prices are volatile necessitating frequent policy changes.

The counter-arguments are the following. First, food inflation impacts both core inflation and overall inflationary expectations. Ignoring it can unanchor inflationary expectations and undo the past successes of IT.

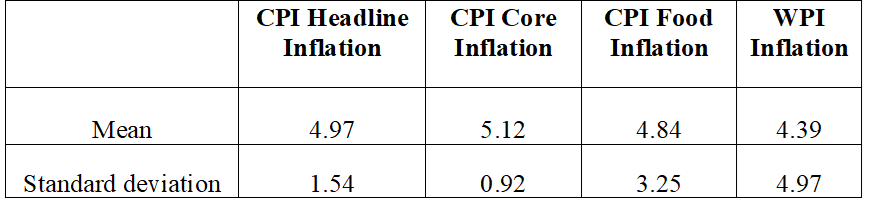

Second, WPI is a poor substitute. It consists of wholesale prices, not retail prices; and of only manufacturing (64 percent weight) and commodities, while excluding services altogether.

Third, food price inflation has not been higher than core inflation. While it has been more volatile than core inflation, but less volatile than WPI inflation.

Table 1: Comparing Average Level and Volatility of

Different Inflation Series during September 2016 – June 2024

Finally, defying some of the earlier scepticism, IT has not made the RBI overly hawkish or reactive to every small deviation in inflation rate from its target of 4 percent or to every spike in food inflation.

Since September 2016, the RBI has changed the key policy rate 17 times, majority of them during two turbulent years. The first time in 2019-20 when the policy rate was eased five times by a cumulative 185 basis points in order to respond to a sharp growth slowdown. And again in 2022-23 when the policy rate was increased six times by a cumulative 210 basis points in response to accelerated inflation emanating from global shocks. During the remaining 6 years, the policy rate was changed only six times, about once every year.

But what if food prices become even more volatile during the coming years, due to climate change- induced heat waves and erratic rain patterns?

The answer lies in updating the CPI headline basket. The current basket accords a weight of 45.8 percent to food. The basket was calculated in 2011-12 and has not been revised since then, even though per capita incomes have nearly doubled meanwhile.

In order to project the correct weight of food in India’s consumption basket, we estimated the relationship between the share of food and per capita income across countries; and a similar relationship for the Indian states. The estimates robustly confirm that the share of food in consumption declines as income levels increase. While a Bangladeshi spends 45 percent on food, a Vietnamese spends 33 percent; a Brazilian 24 percent; and a South Korean only 14 percent. Similar dispersion is seen across Indian states (as of 2011-12).

The estimated weight of food for India at today’s per capita income would be less than 40 percent instead of the current 45.8 percent; and would decline to below 30 percent in a decade from now. This correction itself should ameliorate the concerns on account of food inflation being a part of the inflation target.

Does it mean that India needs no review or revision of its IT framework at all?

Not really. In fact, it would be useful to conduct an independent review around issues such as: Is a 4 percent target inflation still appropriate? Should India make its tolerance band of 2-6 percent narrower? Or should it move from targeting an inflation level within a band, to just targeting a narrower band of say 4-6 percent, with no explicit point target?

The writer is director general of National Council of Applied Economic Research. Views are personal.