8 May, 2026

Published in: Ideas for India

Published in: Ideas for India

In the second part of our series on India’s new labour reforms, Afridi and Thakur focus on the Code on Social Security, 2020 – in terms of its rationale, the key legislative changes that it entails, state-level implementation, and what the existing theoretical and empirical literature says about potential impacts. They contend that it is likely to cause divergence: modest gains in large formal firms, growth-suppressing distortions in small enterprises – along with a majority of informal workers with limited social security benefits.

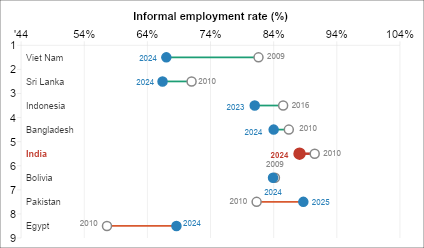

Social security – the provision of a safety net against retirement, health expenses, and income shocks – is a foundational principle of formal employment. In India, this net remains out of reach for most workers. With 88% informally employed in 2024, down only marginally from 91% in 2010 (Figure 1), the vast majority of the workforce lacks pension, health insurance, or any income protection. India’s principal social security schemes (that is, Employees’ Provident Fund (EPF) and Employees’ State Insurance (ESI)) cover formal establishments only above a size threshold, structurally excluding informal, casual, and platform workers.

The Code on Social Security, 2020 is an attempt to address the poor coverage of social security benefits by widening its reach beyond formal establishments, making accumulated benefits portable so workers do not lose protection when they change jobs and bringing gig and platform workers under statutory coverage for the first time.

Figure 1. Informal employment rate: India versus other developing economies

Source: ILO Statistics – Informal employment rate, Total (all sexes); Selected lower-middle income economies.

Notes: (i) Hollow circle = earlier year; Filled circle = latest year. (ii) Short red line (India) = insignificant progress over 14 years despite strong GDP (gross domestic product) growth.

Key changes in the Code on Social Security, 2020

The Code on Social Security, 2020 introduces several structural changes that collectively reshape India’s social security landscape.

First, it consolidates nine separate labour statutes into a single legislation, replacing multiple overlapping inspectorates with a single Inspector-cum-Facilitator and unifying compliance filings – directly lowering the administrative cost of formal employment.

Second, the 50% wage rule closes the most exploited salary-structuring loophole, whereby employers inflated allowances to suppress basic wages and shrink EPF, gratuity, and maternity liabilities; any excluded allowances exceeding half of total remuneration are now reclassified as wages.

Third, a new category of fixed-term employees receive full parity with permanent workers from day one, with gratuity accruing on a pro-rata basis after one year rather than the earlier five-year threshold that effectively excluded the entire contract workforce.

Fourth, gig and platform workers are formally recognised for the first time, with digital aggregators required to contribute between 1% and 2% of annual turnover to a dedicated Social Security Fund.

Fifth, central and state governments are empowered to frame welfare schemes for unorganised workers, while Aadhaar-seeded, Universal Account number (UAN) based portability ensures accumulated benefits are no longer lost when workers change employers or cross state lines.

Sixth, the Code reverses the earlier perverse arrangement whereby employer default could deny workers their benefits – ESIC (Employees’ State Insurance Corporation) may now pay benefits directly and recover the capitalised value from defaulting employers.

Seventh, penalties for non-compliance are substantially stiffer. Finally, wage ceilings and contribution rates can be revised by government notification without fresh legislation, making the framework more responsive to economic change.

State-level implementation

The distribution of states by preparedness for implementation of the new code (Figure2) reveals considerable variation. Early adopters had published draft rules by 2021; a second wave followed in 2022 and after; West Bengal and Tamil Nadu are yet to publish draft rules within the reference period. This uneven adoption reflects India’s federal dynamic – where state capacity, political priorities, and administrative bandwidth determine how quickly central labour legislation translates into operative rules.

Figure 2. State-wise timing of adoption of rules under the Social Security Code

Source: Authors’ compilation based on state government gazette notifications on the Code on Social Security issued by state labour departments (2020-2025).

Notes: The map shows the year in which states and union territories issued draft or final rules under the Code on Social Security, 2020. Where both draft and final rules were notified, the year of the first notification is reported.

Literature review

A review of the existing literature yields divergent predictions on how social security may affect employment and productivity, as the tables below illustrate – the outcome depends critically on firm behaviour, market structure, and institutional design.

Potential impact on employment

Table 1. Theoretical impact of social security on employment

Source: Authors’ compilation.

Evidence from India’s labour market suggests that raising the cost of formal employment consistently drives informalisation. Besley and Burgess (2004) showed that pro-worker amendments to the Industrial Disputes Act reduced formal manufacturing employment while expanding the informal sector. Ahsan and Pages (2009) found that firms typically respond to higher formal labour costs by shifting towards contract and casual arrangements rather than cutting headcount outright.

The most direct evidence on a specific social security component comes from the Maternity Benefit Amendment Act of 2017, which extended paid maternity leave from 12 to 26 weeks for firms with ten or more employees. Banerjee, Biswas and Mazumder (2025) find a decline in employment probability and earnings for targeted women. Bose and Chatterjee (2024) show that women in covered firms were 4.3 percentage points less likely to hold regular salaried jobs and 5.3 percentage points more likely to be in casual or unpaid work. Since the cost falls entirely on employers rather than a shared insurance fund, firms have a strong incentive to reclassify women into ineligible arrangements – meaning the reform measurably harmed those it intended to protect.

Table 2. Theoretical impact of social security on productivity

Source: Authors’ compilation.

India’s experience shows how social security mandates interact with policy distortions to shape productivity through capital deepening. Hasan, Mitra and Sundaram (2013) find that Indian firms employ more capital-intensive production techniques than countries at comparable development stages, attributing this to stringent labour regulation that raises the effective cost of formal employment and induces capital substitution even where factor endowments would counsel otherwise. While this raises measured labour productivity, the gains reflect allocative inefficiency rather than genuine technological progress.

Trade liberalisation can reinforce these dynamics through a complementary channel. Hasan, Mitra and Ramaswamy (2007) show that in states with more restrictive labour laws, firms adjusted to competitive pressure through capital substitution rather than employment flexibility, while Sen and Das (2015) add that trade reforms simultaneously reduced the relative price of capital goods. Regulation raising labour costs and trade reform lowering capital costs thus operated in the same direction, with their combined effect exceeding what either would produce independently.

The structural consequence is a diminished employment margin. Adhvaryu, Chari and Sharma (2013) demonstrate that industrial employment in stricter regulation states is less sensitive to demand shocks, as firms having reorganised production around capital-intensive models no longer expand or contract workforces in response to demand fluctuations – a rigidity with significant implications for inclusive growth

Summary of expected impacts in India

The Code’s effects on employment and productivity depend less on its provisions than on how mandates interact with firm size, labour market structure, and worker perceptions of contributions. On employment, the tiered threshold architecture – EPF at 20 and ESI at 10 workers – may create sharp compliance cliffs that incentivise firms to remain sub-threshold by limiting hiring, fragmenting operations, or substituting contract labour. Where a large informal sector sits outside the regulatory perimeter, tightening formal compliance may lead to informalisation rather than net employment reduction.

On productivity, larger formal firms benefit from reduced worker turnover and skill accumulation, but compliance costs may induce capital substitution that inflates productivity metrics without genuine gains. For small enterprises, threshold incentives may suppress firm growth and foreclose the scale economies that drive long-run productivity.

The overarching prediction on potential impact is divergence: modest gains in large formal firms, growth-suppressing distortions in small enterprises – along with a large share of the workforce engaged in informal work with limited social security benefits.

The views expressed in this post are solely those of the authors, and do not necessarily reflect those of the I4I Editorial Board.