Farmers should be trained in the use of the machinery, while production units must leverage the services of ITIs

The recently released NCAER white paper on ‘Making India a Global Power House in the Farm Machinery Industry’ reveals a mismatch between what the organised industrial sector is producing, especially in the non-tractors segment, and what the small and marginal Indian farmers want.

The farm machinery industry is characterised by both demand and supply-side challenges. Farm mechanisation in India, at 40-45 per cent, remains low compared to the rest of the world; in the US it is 95 per cent, Brazil 75 per cent, and China 57 per cent.

Skills shortage is a problem, resulting in a low-equilibrium trap for the industry. It is not surprising that village craftsmen, who fall at the bottom of the pyramid in the industry, form the largest group and are the ones who end up largely catering to the Indian farmers in terms of supply, repair, and maintenance of farm machinery.

There is a lack of adequate information and awareness amongst farmers about the technology and the management of machinery. Consequently, their selection of machinery is poor, often making it a wasted investment.

On the supply side, micro, small, and medium enterprises (MSMEs) suffer from a lack of skilled personnel. Fabrication of agricultural tools and machinery is often done by semi-skilled workers without proper equipment. In the case of small-scale fabricators, there are hardly any qualihed supervisors to monitor quality. Finding qualihed personnel for testing machinery is also a challenge.

Extension programmes need to be strengthened to address demand-side issues. First, State agricultural universities, ICAR and other institutes that have tractor training centres, Krishi Vigyan Kendras and industry (through their dealers) should be made responsible for training young farmers/owners/operators on how to select, operate and service farm machinery. They should also provide information on developments in mechanisation including the availability of new and better farm equipment for different applications.

The programmes of front-line demonstration of farm machinery should be strengthened. Handheld training to users of new-generation farm machinery may encourage the extension and adoption of farm power.

Bridging the gap

The Agricultural Skills Council of India should work at the district level to address skilling shortages on the demand side; public-private partnerships with Custom Hiring Centres may be especially useful. ICAR institutes can offer short courses that address skills shortages on the demand side and Industrial Training Institutes (ITIs) can be leveraged to address the skill gaps in repair and maintenance.

Service centres at the regional and State levels may be promoted in the private and industrial sectors. This will alleviate the need for each farmer to own machinery and learn skills to operate the individual machines. Each centre can also rent out machines with the associated package of service. Such service enterprises will also create jobs for skilled youth in that region.

On the supply side, the District Industries Centre should work with local industrial clusters so that ITIs can provide relevant courses with the latest available technical knowledge and skills.

Dual vocational skilling programmes will greatly beneht industrial clusters located in tier-II and tier-III cities. MSMEs should also leverage the Apprentices Policy of the Central Government. This may be a win- win situation for the youth.

Bhandari is Professor, and Joshi is Fellow, at NCAER. Views are personal.

Not factoring in climate risk will cost cities dear.

India is one of the fastest growing economies in the world. According to EY forecast, India is expected to be a $26 trillion economy (in market exchange terms) by 2047. The per capita income is expected to increase to $15,000, putting the country among the ranks of developed economies. However, to become a global economic powerhouse, several actions need to be taken.

A critical one concerns the urbanisation process underway in India. The number of inhabitants in Indian cities is estimated to have increased almost fourfold between 1970 and 2018, from 109 million to 460 million. The country is expected to add another 416 million people to its cities by 2050 and have an urban share of population of 50 per cent. Cities in India occupy just 3 per cent of the nation’s land, but their contribution to GDP is a massive 60 per cent.

Many Indian metros are not meeting their potential in serving as engines of economic growth and job creation. Several factors are responsible for this: (i) inadequate investment in urban infrastructure; (ii) fragmentation of responsibilities and limited ownership of economic initiatives between urban local bodies and State government agencies; and (iii) lack of business- and investment-friendly initiatives and regulations in urban and peri-urban areas.

To come up with relevant interventions and frameworks that address these issues, interactions were carried out with government and private sector stakeholders across project States, cities, and other major urban centres in India. Along with the stakeholder consultations, cities in India and abroad were also studied to derive lessons across the areas of: (i) integrated economic vision and planning; (ii) policies, regulations and promotion of investments; and (iii) integrated master planning to enable the integration of land use and infrastructure provision, etc.

While these are important steps, one aspect that is completely left out from our city planning is to make the cities cope with climate risk. IPCC projections suggest that the likelihood of events like extreme precipitation are bound to happen more frequently with climate change. The planning for the cities without factoring this may be too costly.

Unprecedented flooding

For example, Mumbai experienced unprecedented flooding in 2005, causing direct economic damages estimated at almost $2 billion and 500 fatalities as per the study, ‘An assessment of the potential impact of climate change’, published in a climate journal. The findings suggest that by the 2080s an ‘upper bound’ climate scenario could see the likelihood of a 2005-like event more than double. The estimate states that total losses (direct plus indirect) associated with a 1-in-100 year event could triple compared with the current situation (to $690-1,890 million), due to climate change alone.

The analysis also demonstrates that adaptation could significantly reduce future losses. For example, estimates suggest that by improving the drainage system in Mumbai, losses associated with a 1-in-100 year flood event today could be reduced by as much as 70 per cent.

Similar catastrophic events, though on a lower scale, were seen recently in cities like Chennai, Gurugram and Bengaluru. However, city planners do not seem to have learnt the lesson. Ideally, planning for mega cities need to incorporate: assessment of current and future rainfall pattern in megacities; urban flood model/storm water management model; and spatial distribution of people/property and insurance penetration.

AI based modelling is probably the right approach to build scenarios for the medium, long term on these aspects. These may be linked to a city based economic model to quantify the likely cost in the event of occurrence of climate-led disaster in a megacity. An upfront number incorporating all aspects of cost is an important component of an adaptation assessment plan as policymakers could visualise the potential cost of no-action.

The writer is Professor, NCAER. Views are personal

Misdirected. Instead of ‘Big Food’ focus, farmers must be empowered to make millets a vital part of food schemes.

India is at the forefront of an exciting movement to promote millet consumption. Having successfully proposed 2023 as the International Year of Millets to the United Nations, India has positioned itself as the global leader in production, research and innovation of these nutritious grains.

Millets have enormous potential in tackling the country’s concurrent nutritional challenges of widespread ‘hidden hunger’ and high cardio-metabolic disease. However, the strategies being utilised to re-introduce millets as a mainstream staple are misdirected and could result in failure, unless greater thoughtfulness and creativity are exercised now.

Misplaced focus

First, Big Food industry is being encouraged to launch millet-based products by providing sales-based incentives through the Ministry of Food Processing Industries’ Production Linked Incentive Scheme for Millet-Based Products (PLISMBP). The scheme’s aim is to promote the manufacturing of ready-to-eat and ready-to-cook millet-based products.

Food industry conglomerates such as Britannia, Hindustan Unilever, Kellogg, and Nestle India have jumped on board and are developing a range of packaged biscuits, breakfast cereals, instant noodles, powdered beverages, and savoury snacks, all of which are categorised as ultra-processed foods.

Ultra-processed foods are those which are composed of ingredients that are extracted from whole foods utilising industrial processing techniques. They usually have added sugar, salt, and fat, as well as flavour enhancers, artificial colouring, stabilisers, and preservatives to make the product hyper-palatable and prolong shelf life.

Ultra-processing of millets is not the solution to promoting their use. In fact, it will be harmful. The evidence is clear — consumption of ultra-processed foods increases the risk of obesity, cardiovascular disease, metabolic syndrome, depression, and premature mortality. The popularity of such foods has been increasing rapidly in India, among all income groups, in both rural and urban areas. One study of adolescents in Delhi found that up to 20 per cent of daily calorie intake comes from ultra-processed foods.

Second, is large investments in the start-up space to develop millet-based products. Unlike sales-based incentives, the Nutrihub incubator of the Indian Institute of Millets Research offers seed funding to nutricereal entrepreneurs at the idea and prototype stages, as well as training, mentoring, access to investor networks, and use of R&D facilities. Many of these start-ups brand themselves as ‘clean food’ and thus manufacture products that are free from artificial ingredients and additives. But, they are also prohibitively priced. The once ‘poor man’s food’ is now clearly marketed to the urban elite.

There is a disconnect between what has been termed the ‘People’s Movement’ — evocative of a crusade for food sovereignty to empower farmers and revitalise the forgotten, traditional millet — and the reality of where this campaign is potentially headed — into the pockets of Big Food, and the plates of the well-off.

What is missing from the strategy is a strong push from the Centre to mainstream millets into the pillars of the National Food Security Act. Millets are often hailed as the ‘key’ to solving India’s food insecurity, especially in the face of climate uncertainty, yet they are far from being a fundamental component of the country’s food security schemes.

Prioritising the consumer

Recognise the power of India’s culinary backbone — street food: On the one end, farmers are being urged to increase production of millets, and at the other end, Big Food and start-ups are being incentivised to manufacture millet-based packaged goods. There is a gaping hole in the middle which includes those who source ingredients to produce fresh and lesser processed foods — street vendors and small-scale food outlets.

These business owners can actually deliver millets to the masses in a healthier way. Consider, for example, puffed jowar bhel, ragi tikki chaat, or bajra ladoos. Can existing incentive-based schemes be inclusive of innovative vendors and creative dhaba chefs to promote affordable and accessible millet-based offerings? Street food is, after all, the original RTE, just without all of the packaging and intellectual property.

Understand and respond to rural preferences: India is still 65 per cent rural. For millets to truly become the staple food they once were, they must be not only accessible, but demanded by rural populations. The only studies on knowledge, attitudes, and practices surrounding millets are from urban India.

A recent, multi-city study found the top reason for consuming millets was because of an existing health problem such as diabetes.

Findings from the urban context may have little relevance in rural areas, where non-communicable diseases are under-diagnosed. Additionally, millets hold significance in many rural areas as animal feed, so preferences need to be researched and understood before launching awareness campaigns and millet mahotsavs to tailor messaging appropriately.

Regulate advertising and labelling of millet-based products: PLISMBP guidelines state that public funds will be provided for sales of millet-based products that contain at least 15 per cent millet.

This means the remaining 85 per cent can include ingredients such refined white flour, hydrogenated fats, sugar, and additives, yet in all likelihood will still be marketed as a health food to consumers. One only needs to look as far as Oats Instant Noodles — labelled as ‘nutrilicious’ — or Quinoa Puffs — advertised as a diet snack — for examples of super-foods perhaps gone wrong. Big Food advertising and labelling must be regulated before millets become a nutritional disaster.

We will do well to remember that rice and wheat did not come to dominate our plates through heavy promotions, celebrity endorsements, and global campaigns, but rather structural policies that ensured profitability for farmers and affordability for consumers.

During his post-monetary policy media interaction last week, RBI Governor Shaktikanta Das declared that the central bank has paused, not pivoted. After raising interest rates by a cumulative 250 bps, in six consecutive meetings during the period May 2022-February 2023, the RBI decided to keep the policy rate unchanged in its first monetary policy meeting of 2023-24. Simultaneously, it reiterated its commitment to bring inflation down to 4 per cent from the current level of about 6 per cent.

Why did the RBI pause its tightening streak? What would be its future course of action: will it continue to pause; raise; or lower the policy rates in the coming months?

The recent pause can be attributed to a number of factors. First, the Indian economy seems remarkably resilient despite persistent global turmoil manifested in the stubbornly high inflation in advanced economies; multi-decadal high interest rates; a banking crisis, which was thankfully contained; and sequential growth downgrades.

The RBI has upgraded projections for GDP growth for 2023-24 slightly to 6.5 per cent from 6.4 per cent; and has lowered the projected inflation to 5.2 per cent from 5.3 per cent. In addition, the banks and Non-banking Financial Corporations (NBFCs) are holding up well on asset quality; the exchange rate has stabilised; and the volatility of capital flows has subsided. The latter has enabled the RBI to build its forex reserve buffer back to the $ 600 billion-odd level.

In the absence of any compelling reasons for a monetary policy action, a pause seems like an eminently sensible decision.

Second, given the lag with which the full transmission of monetary policy takes place, it would be appropriate to allow time for the past rate hikes to work their way through the system. For example, till date, banks have transmitted only about half of the past rate hikes into deposit and lending rates. The transmission through other formal and informal financing channels has also likely been incomplete.

Third, given the pervasive high inflation rates and negative policy interest rates in the advanced economies, the RBI’s inaction with inflation hovering around 6 percent carries very little credibility risk. Besides, the decline in household inflationary expectations has boosted the RBI’s credibility further and will assist in keeping inflationary expectations anchored.

In order to anticipate RBI’s future course of action, one needs to look beyond short run, cyclical considerations. Instead, it would be useful to analyze the evolution of RBI’s approach toward monetary policy over the past several years; including the relative weights attached to inflation and growth.

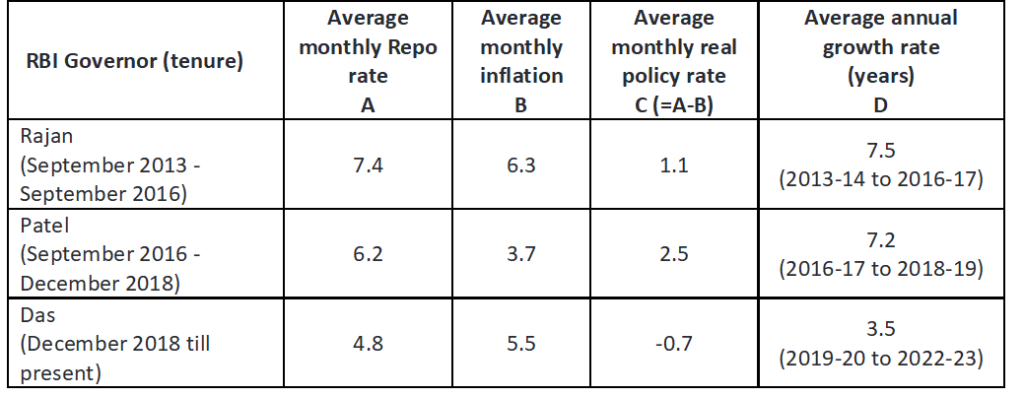

A comparison of the average monthly inflation rate, repo rate, and real interest rate, during the consecutive tenures of RBI Governor(s) Raghuram Rajan, Urjit Patel, and Shaktikanta Das offers interesting insights (see Table 1).

Table 1: Inflation, Growth Rates, Interest Rates, and Real Interest Rates during Different Regimes

Both inflation and policy rates were high during Rajan’s tenure during September 2013-September 2016, averaging 6.3 per cent and 7.4 per cent respectively, resulting in an average real interest rate of 1.1 per cent.

Inflation declined drastically during Patel’s tenure (September 2016 – December 2018), but the repo rate did not decline as rapidly. Consequently, the real interest rates more than doubled to 2.5 per cent. The annual GDP growth rate was slightly slower during Patel’s tenure, suggesting a hawkish regime.

The tenure of Governor Das, since December 2018, has coincided with a polycrisis resulting in a sharply decelerated average GDP; and elevated inflation. Despite average monthly inflation accelerating to 5.5 per cent, the policy rate has declined, yielding a negative real interest rate.

Evidently, the RBI has pivoted monetary policy to address concerns related to growth more than those concerning inflation in recent years.

Currently, risks to growth outweigh risks to inflation, both globally as well as in India. The RBI will either continue to pause or will cut rates during coming months, if such risks to growth materialise. It is unlikely to tighten even if inflation remains at the 5.25-5.5 ballpark level.

In its recent actions, the RBI seems to have resolutely pivoted toward a more flexible interpretation of the inflation targeting regime, than has been the case in the past.

It should serve the economy well under the circumstances.

India is achieving significant strength in the allied space of agriculture. Fishery, dairy, and livestock are the areas of livelihood support for the millions. Moreover, India’s nutritional and food securities are deeply rooted in this sector.

Among the allied activities of agriculture, the fishery is growing at a higher pace and is recognized as a ‘Sunrise Sector’ with an outstanding double-digit average annual growth of production, which is 10.3 per cent in 2021-22.

A record fish production of over 15 million tons in 2021-22 has revealed a huge potential for the future. Moreover, it helps sustain the livelihood of over 28 million people in India of which the marginalized and vulnerable communities have a commendable level of participation

India is the second largest fish-producing country in the world accounting for 7.6 per cent of global production and contributing about 7.3 per cent to the agricultural Gross Value Added (GVA) of India. Fish being a rich source of animal protein, is one of the healthiest options to mitigate hunger and nutritive deficiency.

However, the fishery sector is beset with a few major problems, which have been noted in the recent National Council of Applied Economic Research (NCAER) study (March 2023) of the fishery sector for the Department of Fishery of Government of India. The primary survey of NCAER covered 12600 fish-eating households in 105 districts across 24 states of India.

Among the major problems, the price factor remains a critical dent in its accessibility to the less affordable. In terms of expenditure quintiles of household, the consumption of fish (with 30 days reference period) reveals almost a linear distribution, with richer quintiles of households consuming a higher average quantity of fish, while the poorer the less. As shown in the graph below (Figure 1), the poorest households consume less fish compared to the richest.

The distribution of expenditure groups and the consumption of fish (in kg) in a 30-day reference period is shown in the following Figure.

Figure 1: Consumption inequality of fish among expenditure groups in quintiles

Source: NCAER Primary Survey

The nutritional value of fish is enormously important. . The growth of organized food retail markets, food-tech services and eating-out trends have an impact on the demand for fish and fish products. This growth is further fuelled by the shifting of policy level focus from ‘food security’ to ‘nutrition security’.

However, as already mentioned, a large number of households remained bereft of fish consumption just because of affordability. There are states where fish demand is more, whereas there are states where production far surpasses consumption. The states with less per capita income tend to have higher distress with respect to the price of fish.

A high price is reflected to be the critical restricting factor for the consumption of fish by fish-eating households in several states. It may be noted that states where high price deters consumption of fish are the ones having a high propensity to consume.

At all-India levels, 73 per cent of the households observed high prices as the steepest restricting factor. It may be noted that states with less per capita income are the ones which impacted their consumption more due to prices. High-income states like Delhi, Goa, Tamil Nadu, and Karnataka are far below the national average, showing better affordability of the fish-eating households in this state.

The state-level distribution is important to gauge the level of consumption which shows the inequality of consumption of fish. Therefore, proper distribution from the surplus production area to the ones where consumer demand is more should be the priority to lower the price constraint and enhance the level of fish consumption.

This will, in turn, help enhance the per capita consumption of fish to a higher trajectory. Moreover, there is a very poor mechanism for the preservation and transportation of fish to bridge the supply-demand gap.

Figure 2: High price is the restraining factor in most low-income states, leading to inequality of consumption of fish among states

Source: NCAER Primary Survey, Per Capita Income of States is sourced from Reserve Bank of India; Note: PCI=Per Capita Income at Constant 2011-12 prices

The above-mentioned price restraining factor among state households critically points out the inequality of consumption of fish among quintiles of the expenditure groups as well in the states with a higher proportion of fish-eating households.

How the consumption inequality could be redressed? It is a fact that supply-side aspects should play a critical role in reducing consumption inequality as noted above.

India is a production surplus country and aquaculture has immense possibilities. However, the fish market in India is mostly unorganised and lacks scientific preservation mechanisms and better transportation, impacting supply from the surplus-producing states to the deficit areas.

The budgetary allocation for the Department of Fisheries has gone up by a whopping 38.5 per cent to Rs. 2248.8 crores as against the corresponding figure of Rs. 1624.2 crores during 2022-23. This is one of the highest-ever annual budgetary support for the Department.

Emphasis is now placed more on the formalization of the sector, encompassing digital inclusion, simplifying access to institutional finance for capital investment and working capital, and providing incentives to microenterprises operating in the fisheries and aquaculture sector to work on value-chain efficiencies.

Reassuring micro and small enterprises to establish supply chains for delivery of safe fish products to consumers, thus expanding the domestic market and incentives for the creation and maintenance of jobs for women in the sector.

Physical accessibility and economic accessibility of fish to consumers need to be addressed in a balanced way to boost the demand. In some rural areas, fish is available only in the weekly market and not available daily, thereby limiting its consumption.

Mobile fish vending vehicles, introducing fish retailing in rural areas, etc. will improve the accessibility of fish to consumers. Mobile fish vending should be promoted by extending financial support for cycles with ice boxes, motorcycles with ice boxes, and three-wheeler with ice boxes including e-rickshaws.

Fish transport vehicles/facilities procured under the scheme should be used only for transporting and marketing fish and not for any other purposes. Therefore, the demand-side aspects need complementary support from the supply side to enhance access to the market.

The fisheries sector lacks an extensive temperature-controlled supply chain from harvest to consumption. The challenge is more so in the domestic sector, where the marketing of fish and fish products is highly unorganized and unregulated. Further, fish production is not evenly spread across the country, and major production is limited to some states.

Hygienic distribution of fish and fish products (chilled fresh, dried or processed) across the states to meet the growing demand of fish deficit states including those in the NE region where fish is a predominant source of protein continues to be a challenge.

With improved infrastructure and strengthening of the supply chain, the fishery could emerge as a crucial substitution for chicken and competitive, just like aquatic chicken (Tilapia) even for high-value fish with other alternatives. According to the UN-FAO, this variety of fish is one of the fastest-growing farmed fish around the world, and along with carp and catfish, it will take a share of more than 60 per cent of the total global farmed fish production.

In India, the general acceptability of frozen fish amongst consumers is poor as compared to fresh fish. Consumers often suspect the quality of frozen fish and it is somewhat true as India lacks a robust integrated cold chain supply system for fish and fish products.

The government should prioritize the promotion of integrated cold chains (ICCs) by extending financial assistance and facilitation for the establishment of key cold chain infrastructure facilities such as chilled storage facilities, ice plants, cold rooms, freezing units, value addition unit operations, reefer transportation, modern air-conditioned retail outlets and implementation of modern sanitary and hygienic practices etc.

This initiative has the potential to improve efficiency in handling, storage, transportation and marketing of fish and fish products besides reduction in post-harvest losses and meet growing and continued demand for the supply of safe and nutritious fish to consumers at reasonable prices. Overall, it can lead to enhanced per capita fish consumption contributing to the nutritional security of the country.

There is also a need to identify water bodies under aquaculture that are unsuitable for intensive cultivation and guide them towards optimizing their production for producing fresh fish in an economic manner for the domestic market.

Contract farming models may be promoted to achieve better integration among fish farmers and processors. Contract fish farming is a type of aquaculture where a company contracts the farmers to raise fish for them. The company provides the farmers with fingerlings, feed, and technical assistance.

The farmers are responsible for raising the fish to market size and delivering them to the company. It can be seen as a way for small-scale farmers to get involved in aquaculture without making a large investment.

The feasibility of contract farming and buyback arrangements should be explored in aquaculture wherever appropriate and feasible. It will ensure an assured market for the producer as well as better quality products for the consumers. With a better supply scenario in place, the price will soften to include more consumers.

Saurabh Bandyopadhyay, Senior Fellow; Nijara Deka, Associate Fellow; Palash Baruah, Associate Fellow; Laxmi Joshi, Fellow; Falak Naz, Research Analyst at NCAER. Views are personal.