India’s economy may stay in a low equilibrium if we do not act to resolve well identified restraints on women taking up employment. A comparison of urban and rural data shows that neither setting is working for women, even if the reasons differ.

As India inches closer to the $5 trillion economy mark with human capital playing a key role, a critical disconnect emerges in this growth story: the disparate contribution of women to the labour force and the economic loss therein.

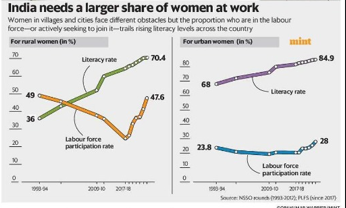

According to the Periodic Labour Force Survey (PLFS) 2023-24, the literacy rate for urban women stood at 84.9%; yet their labour force participation rate (FLFPR) was only 28%. In contrast, the gap between literacy and work participation for rural women is smaller at 22 percentage points (see data graph).

While this imbalance is universal, even among developed economies like the US, Japan, Germany and Australia where female literacy rates are nearly 100%, there is an almost 40 percentage point gap between literacy and FLFPR (World Bank 2024).

However, developing nations like Vietnam and Bangladesh show a smaller gap of 25 points. India lies in between, with a gap of nearly 33 points (rural-urban combined) but with a lower female literacy rate (74.6% according to PLFS 2023-24).

This reveals a deeper structural and social disconnect that continues to limit women’s economic engagement. Without addressing this gap, our growth milestones risk becoming superficial targets.

This leads us to a deeper question: Are rural women conditioned to seek rural employment over urban or is urban planning failing women?

The differing socio-economic and infrastructural contexts of rural and urban India, perceived as two distinct worlds, shape female labour force outcomes in contrasting ways.

According to PLFS 2023-24, over 92% rural women workers were either self-employed (73.5%) or casual labourers (18.7%), predominantly engaged in agriculture.

In contrast, only 42.3% urban women were self-employed, seeking jobs in the services sector, a domain that—as the World Bank notes—offers women limited returns due to persistent barriers such as restricted mobility, informal work arrangements, concerns around workplace safety and prevailing social norms (South Asia Development Update, 2024).

These structural challenges contribute to what McKinsey described in 2018 as a “leaky pipeline,” where women enter the workforce but steadily drop out before reaching mid- and senior-level roles.

Further compounding this challenge is the role of caregiving, with national data showing women with young children were significantly less likely to be employed (Chatterjee, Desai & Vanneman, 2018; India Human Development Survey).

This effects an often irreversible FLFPR loss, evident among women with school-going children. One pertinent factor driving this trend is the lack of accessible and affordable childcare infrastructure in urban India.

Urban settings—where, according to the National Family Health Survey-5, 61.3% urban households are nuclear—often leave women without the familial support needed to balance caregiving and employment.

In contrast, rural India offers stronger community and family networks that help shoulder childcare responsibilities (Bhindi & Jangra, 2025).

Additionally, flexible work options such as self-employment and agricultural labour are more readily available in rural areas, enabling women to balance paid work and childcare through what Gautham (2022) terms the ‘It takes a village’ effect, unlike the rigid and demanding structure of the urban services sector, which offers fewer adaptable opportunities for working mothers.

There was a notable decline in labour force participation among rural women between 2005 and 2019.

This trend is particularly surprising when viewed against the backdrop of falling fertility rates, increasing consumption, rising household incomes and ongoing urbanization, as these are factors that should in theory support greater female participation.

So why have we seen the opposite?

As household incomes rise, deep-rooted cultural norms can take precedence, reinforcing traditional ideas that cast men as breadwinners and women as caregivers. If the financial need for a woman’s income diminishes, her economic participation can reduce further.

India’s rural FLFPR is persistently higher than its urban FLFPR, despite the latter’s education and infrastructural back-up. Instead, what seems to grow with urbanization is invisible labour.

According to the Time Use Survey 2024, Indian women spend an average of 289 minutes per day on unpaid domestic work, compared to 88 minutes for men.

Urban women, in particular, are burdened with the challenge of juggling professional and domestic responsibilities, often without structural support.

This invisible weight leads to time-bound underemployment, where women may want to work but are unable to find opportunities that align with their caregiving obligations.

These unobserved nuances continue to hold back industrious female employment, both in rural and urban landscapes. Further, the post-covid rise in our rural FLFPR can be partially attributed to crisis-driven fallback strategies, uncharacteristic of provident long-term solutions.

The World Bank estimates that closing the gender gap in employment could boost global GDP by more than 20% (Women, Business and the Law, 2024). But this is as much about equity as it is about lost opportunity.

Increasing the FLFPR can make gender progress a key factor in economic output, address issues that women and children face, and enhance social development overall.

This requires redesigning our labour market with investments in public childcare infrastructure, promoting flexible work models and challenging the notion of caregiving as a woman’s exclusive burden as a few of the necessary steps.

A comparison of rural and urban data shows that neither setting is working for women, even if the reasons for this differ. We need to address our low women’s labour force participation to avert a growth story that may remain stuck in a low equilibrium.

The authors are, respectively, research associate and associate fellow, National Council of Applied Economic Research. Views are personal