In principle, a country that relies heavily on economic transactions with countries with diverging geopolitical views is at greater risk of geopolitical disruptions. But risk may also turn to opportunity: a country that interacts with a wide range of partner countries with diverse geopolitical leanings might be more resilient to disruptions from individual partner countries, and might even benefit due to trade or FDI diversion from rival blocs. Gopinath et al. (2024) call such countries ‘connectors’.

In a recent paper (Aiyar and Ohnsorge 2024), we formalise the concept of connectedness as the property of transacting with international partners drawn from across the ideological spectrum, and discuss some examples of connector countries. We also show that more open and financially developed countries tend to be more connected.

Data and methodology

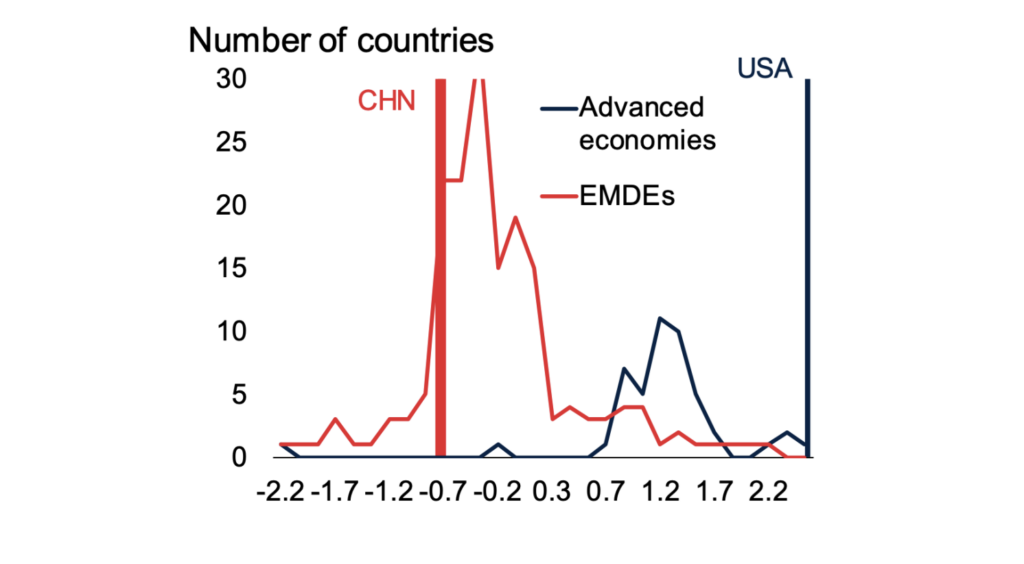

Following Aiyar et al. (2023b) and Gopinath et al. (2024), we use data on voting patterns at the United Nations to measure a country’s geopolitical stance. Specifically, we employ the ideal point index calculated by Bailey et al. (2017). Broadly speaking, over the past decade countries’ geopolitical stances have been clustered into two camps: emerging market and developing economies (EMDEs) and advanced economies (Figure 1). Most EMDEs have voting patterns similar to China, while most advanced economies have voting patterns somewhere between the US and China, but closer to the US.

Figure 1 Distribution of geopolitical stances, 2023

The ideal point distance (IPD) between two countries at any given point in time measures bilateral ‘geopolitical distance’. We combine this with bilateral data on trade (primarily from CEPII and the IMF’s Direction of Trade Statistics), foreign direct investment (FDI, mainly from the IMF’s Coordinated Direct Investment Survey and the OECD), portfolio liabilities (from the IMF’s Coordinated Portfolio Investment Survey), and cross-border bank liabilities (from BIS Consolidated Banking Statistics). The resulting database is available at Harvard Dataverse.

Previous papers, based on proprietary databases, have shown that an increase in geopolitical distance between a pair of countries is associated with diminished bilateral transactions (e.g. Aiyar et al. 2023b for FDI, and Gopinath et al. 2024 for trade). We find greater geopolitical distance is associated with significantly diminished transactions across all categories. The effect is strongest for FDI, with more muted effects for capital goods exports, portfolio investment liabilities, and liabilities to BIS-reporting banks.

Geoeconomic vulnerability and geoeconomic connectedness

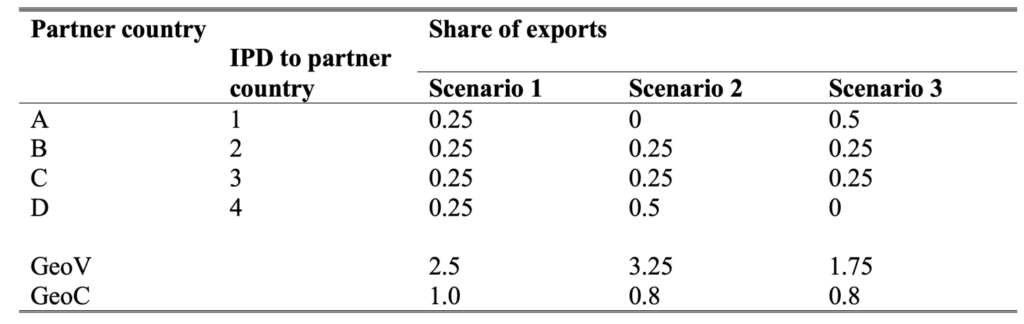

Following IMF (2023), we create an index of geoeconomic vulnerability, GeoV, that is defined as the transaction-weighted average of geopolitical distances. Thus, for example, Mexico’s GeoV for exports is calculated by multiplying its IPD vis-vis a given country by the share of Mexico’s exports to that country, and then summing over countries. GeoV captures the intuition that the more a country transacts with geopolitically distant countries, the greater its vulnerability to a geopolitical shock.

But, of course, this simple weighted average is only one aspect of a more complicated story. In a geopolitically fragmented world, it may not be wise to put all one’s eggs in a single basket. While a country may have a low probability of being hit by a geopolitical shock if it only trades with one politically aligned partner, it would be devastated if a shock actually materialises. From this perspective, diversifying transactions across partners drawn from a range of geopolitical preferences could build resilience to shocks.

We construct an index of geoeconomic connectedness, GeoC, based on the weighted standard deviation of a country’s geopolitical distance from partner countries. Roughly speaking, this means that a country is more connected if its transactions are balanced across many partners drawn from the full range of ideological preferences. GeoC has several attractive properties apart from its simplicity; it uses all the bilateral data available, and does not require any assumptions about which countries belong to which blocs. To the best of our knowledge, it is the first quantitative proposal for measuring how connected a country is in the geopolitical sphere, in a way that is comparable across countries, across time, and across types of transactions.

The difference between GeoV and GeoC is illustrated by the simple example in Table 1. Suppose that a country initially trades equally with four partner countries, at varying geopolitical distances. Now suppose that the country reduces its trade with the geopolitically closest partner, while increasing its trade with the most geopolitically distant partner. Clearly, this increases geoeconomic vulnerability. Conversely, if it increases its trade weight with the geopolitically closest partner, while reducing its trade weight with the most geopolitically distant partner, this reduces geoeconomic vulnerability. But connectedness is reduced in either case, because the country now transacts with a more geopolitically concentrated set of countries.

Table 1 Interpretation of GeoV and GeoC

‘Vertical’ versus ‘horizontal’ connectors: Mexico vs Vietnam

In principle, one could think of connector countries as connectors across markets or connectors across types of transaction.

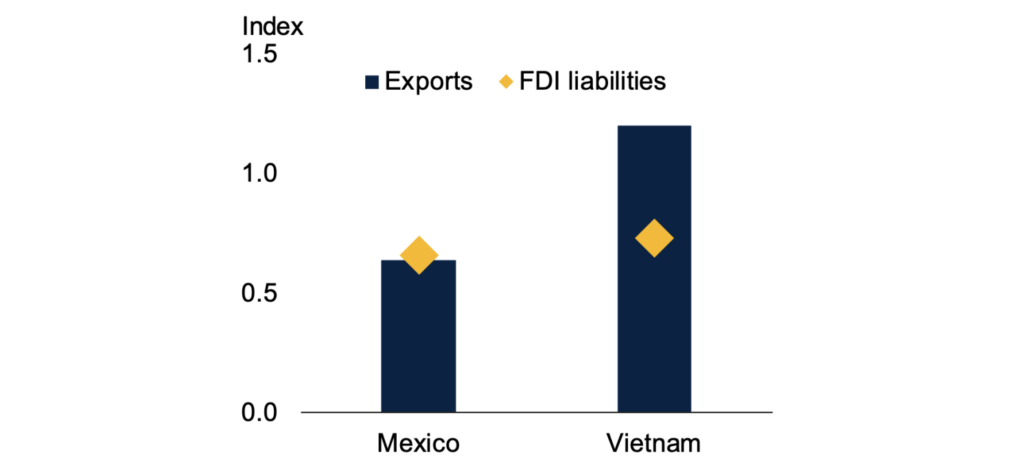

Consider Mexico and Vietnam. Both have a similar degree of FDI diversification. However, Mexico’s exports are overwhelmingly to a single country, the US, whereas Vietnam’s exports are among the most diversified for EMDEs (Figure 2).

When authors such as Gopinath et al. (2024) or Alfaro and Chor (2023) refer to Mexico as a connector country, they are appealing to the concept of connectors across types of transactions in particular supply chains, akin to a ‘vertical connector’: the idea that Mexico will increasingly use Chinese FDI to produce exports for the US market, thus substituting for direct Chinese exports to the US.

But whether this type of connector will gain traction at scale is a matter of some doubt. Republican presidential nominee Donald Trump, in his speech at the Republican National Convention, stated: “[a]nd right now as we speak, large factories, just started, are being built across the border in Mexico. [T]hey’re being built by China to make cars and to sell them into our country, no tax, no anything…[W]e’re going to bring back car manufacturing and we’re going to bring it back fast.” (New York Times 2024). Similar sentiments have been expressed in more guarded language by Katherine Tai, the Biden administration’s trade representative (Associated Press 2024).

In contrast, Vietnam’s highly diversified base of export destinations, akin to a ‘horizontal connector’, gives it some protection against geopolitical risk. If a geopolitical shock were to cut it off suddenly from one export partner, it would have many other partners to turn to. It is therefore a connector across markets. Since this is the conceptual underpinning of our metric of connectedness, Vietnam has a much higher GeoC than Mexico.

Figure 2 Geoeconomic connectedness of Mexican and Vietnamese exports and FDI liabilities, latest

Correlates of connectedness

Which countries are more connected across ideologically disparate partners, thus enabling them to develop some degree of resilience to growing geopolitical fragmentation?

We find that openness is important along several dimensions. A country’s exports are more geoeconomically connected when tariffs are lower and when the country is part of a larger free trade area. Higher-quality logistics – including the ability to track and trace shipments, fewer delays at ports, better trade and transport infrastructure, and more streamlined customs procedures – are also beneficial. And EMDEs with more open capital accounts tend to attract more diversified sources of capital inflows.

Financial market development is particularly important for diversified capital inflows. Deeper and more sophisticated financial markets and institutions facilitate entry and exit and are associated with greater connectedness in FDI, portfolio liabilities, and lending from global banks.

It should be noted that these correlates of greater connectedness are just that – correlates. More research would be required to establish a causal relationship between policy variables and the ability to flourish in a geoeconomically fragmented world. We hope that our work provides a useful first step.