12 March, 2025

India’s rapid economic ascent has positioned it as the world’s fifth-largest economy, with the International Monetary Fund (IMF) projecting it will reach third place by 2027. The Indian government’s ambitious goal of achieving developed-country status by 2047 requires an annual nominal GDP growth of around 10% in USD terms over the next 25 years—exceeding the 7% average of the past decade.

Sustaining this accelerated growth necessitates substantial financing, sometimes externally sourced. Economic history offers cautionary tales: Russia in the early 2000s, Brazil in the 2010s, and China in the 2020s faced macro financial shocks that disrupted their growth trajectories. Such shocks are especially destabilizing when they stem from financing-related vulnerabilities, restricting access to the essential capital required to sustain long-term growth.

India’s external sector appears robust, underpinned by rising foreign exchange reserves and a low external debt-to-GDP ratio—key indicators of macroeconomic stability. However, a closer examination of firm-level data reveals an emerging vulnerability: small and medium-sized enterprises (SMEs) are increasingly accumulating unhedged foreign exchange (FX) exposures. The risks are also found to be especially amplified for financially distressed firms and state-owned enterprises (SOEs). While this risk remains contained at present, its continued expansion could amplify financial fragilities, heightening systemic risk over time and undermining India’s long-term growth trajectory

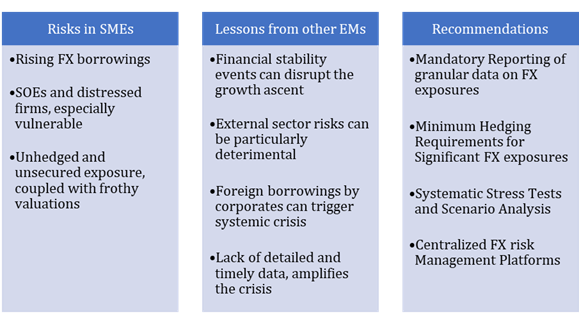

SMEs: A Growing Source of FX Risk

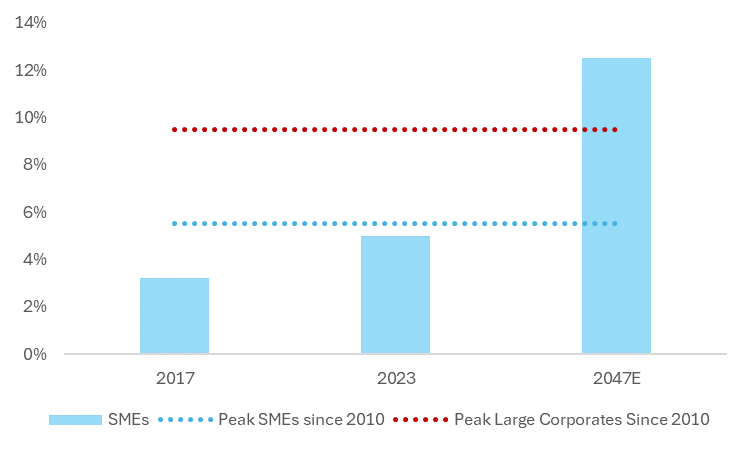

SMEs—defined as firms with assets up to USD 750 million—are integral to India’s expanding economic base, contributing significantly to employment, exports, and supply chain resilience. Despite the presence of a well-developed banking and non-banking financial system, SMEs are increasingly turning to external commercial borrowings (ECBs) to meet their funding needs. Their share of ECBs in total borrowings has surged by 50% over the past six years, reaching 5%. While this level remains manageable today, projections indicate that ECBs could account for 12% of SME borrowings by 2047—a historically high and potentially systemic level.

This shift toward external financing is driven by both push and pull factors. On the push side, domestic credit constraints, particularly for SMEs with limited collateral or weak credit histories, have made access to affordable long-term financing more challenging. India’s banking sector, while relatively stable, remains cautious in lending to SMEs due to concerns over asset quality, higher default risks, and stringent regulatory capital requirements. Additionally, India’s non-banking financial companies (NBFCs), which traditionally played a key role in SME financing, have faced liquidity constraints following periodic stress episodes in the sector.

On the pull side, global financial conditions and market-driven incentives have made ECBs more attractive. Historically low interest rates in international markets over the past decade, coupled with improved sovereign credit ratings and India’s growing integration into global financial markets, have enabled even mid-sized firms to tap offshore borrowing at competitive rates. Furthermore, the flexibility of ECBs—offering longer tenures, reduced documentation requirements, and, in some cases, more favorable repayment structures—has made them an appealing alternative to domestic bank loans. The liberalization of India’s external borrowing framework, including relaxed end-use restrictions and increased access to foreign lenders, has further facilitated this trend.

While external borrowing provides SMEs with a critical avenue to scale operations and invest in growth, the increasing reliance on unhedged foreign debt introduces significant currency and refinancing risks. As global interest rates are starting to normalize and currency volatility is on the rise, the cost of servicing FX liabilities could rise sharply, posing a broader challenge to macro financial stability if left unaddressed

Chart 1: External Commercial Borrowings as a Percentage of Total Long-Term Borrowings

Source: Prowess, Bloomberg, Author Calculations

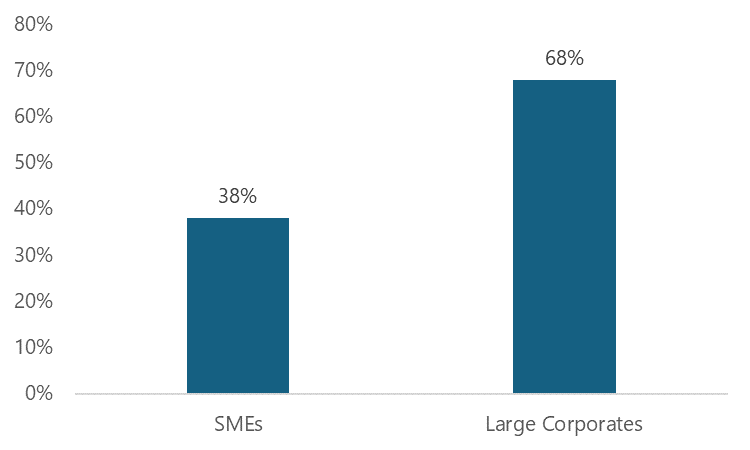

As highlighted earlier, a significant portion of these foreign borrowings remains both unsecured and unhedged, amplifying SMEs’ exposure to currency risk. As of 2023, only 38% of SME FX exposure was hedged, compared to 68% for large corporates—a stark disparity that underscores the urgent need for targeted risk management interventions. This growing vulnerability is particularly concerning as SMEs are currently trading at elevated valuation levels, which could mask underlying financial fragilities.

The current trend bears striking similarities to vulnerabilities observed during the Asian Financial Crisis, particularly in South Korea and Thailand, where currency depreciation, rollover risk, and duration mismatches among SMEs led to severe financial instability. In the run-up to the crisis, many Korean SMEs had accumulated large amounts of short-term foreign currency debt, assuming continued exchange rate stability. However, when the Korean won depreciated by nearly 50 percent, firms with unhedged USD and JPY exposures saw their debt burdens soar, triggering widespread defaults. Compounding the issue, many of these firms faced rollover risk, as creditors became unwilling to extend financing, leading to a liquidity crunch that deepened the crisis.

Thailand faced a similar trajectory, where inadequate FX hedging and excessive reliance on short-term foreign debt led to massive corporate distress when the baht collapsed in 1997. A critical issue in both Korea and Thailand was the lack of granular, real-time data on corporate FX exposures, making it difficult for regulators to assess vulnerabilities before they escalated.

A similar data gap persists in India today. While aggregate indicators—such as foreign exchange reserves and external debt-to-GDP ratios—suggest resilience, firm-level FX risk exposure remains opaque, particularly for SMEs. Without better disclosure requirements and enhanced regulatory oversight, Indian policymakers risk underestimating the potential fragilities building up in the SME sector.

Addressing these challenges requires stronger FX risk monitoring frameworks, stress testing for rollover risks, and incentives for SMEs to adopt prudent hedging strategies. Without proactive intervention, India’s rising SME FX exposures could amplify systemic risks in future episodes of external volatility, much like the Korean and Thai experiences during the 1990s.

Chart 2: Proportion of Corporates Hedging FX Exposure

Source: Prowess, Author Calculations

SOEs and Financially Distressed Firms: Amplification of Risk

Our preliminary analysis, presented in this co-authored blog, offers early insights from our forthcoming research paper, which examines patterns of unsecured foreign borrowing in India’s corporate sector. The findings highlight trends that warrant closer scrutiny, particularly concerning financial vulnerabilities among highly leveraged firms.

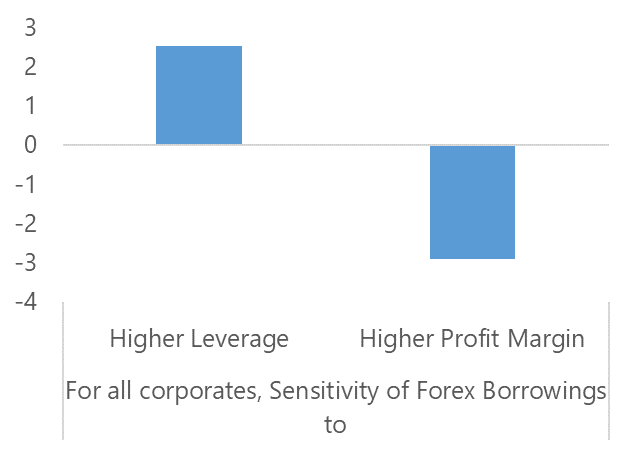

We find that unsecured foreign borrowing is disproportionately concentrated among firms already under financial distress—those with higher leverage and weaker profitability. This trend is especially pronounced among state-owned enterprises (SOEs), which exhibit greater sensitivity to leverage shocks compared to private firms. The tendency of SOEs to engage in riskier borrowing practices may stem from weaker financial discipline, implicit expectations of sovereign backing, or preferential access to credit that is not always aligned with market fundamentals.

Brazil’s experience in the 2010s offers a cautionary lesson. During this period, many Brazilian SOEs became heavily reliant on unsecured foreign borrowings, assuming continued currency stability. However, when the Brazilian real depreciated sharply, these entities suffered significant losses, triggering broader financial distress. The inability to roll over foreign debt, coupled with rising interest costs, forced large-scale interventions to stabilize key sectors. India must learn from such examples and implement stronger risk management frameworks to prevent similar vulnerabilities from emerging within its SOE sector and financially weaker firms.

This underscores the urgent need for improved oversight of corporate FX exposures, stress testing for highly leveraged entities, and proactive hedging strategies, particularly for firms with systemic relevance. Strengthening regulatory frameworks and corporate governance practices will be crucial to ensuring that India’s external financing strategy does not become a source of macroeconomic instability.

Chart 3: Sensitivity of FX Borrowings to Key Fundamental Factors

Source: Prowess, Author Calculations.

Note: The analysis captures the sensitivity of foreign borrowings relative to total borrowings, leverage levels, and market-based profitability projections.

Chart 4: India vs. Emerging Market Peers on FX Exposure

Stakeholder Roles and Key Considerations

Strengthening FX Risk Management: Lessons from Global Experiences

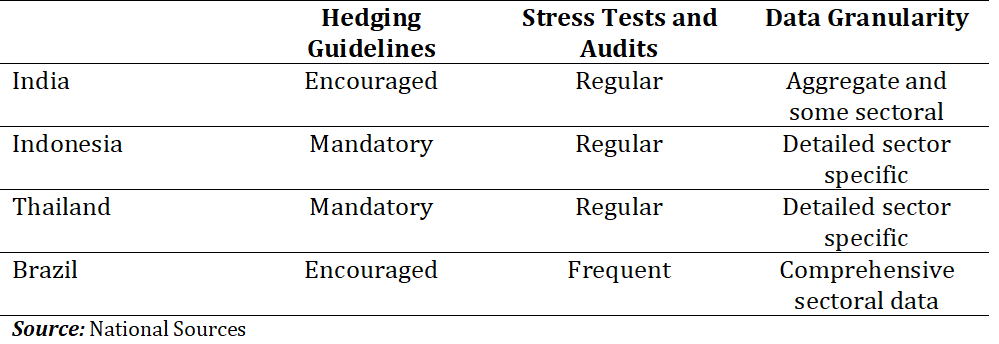

India’s increasing exposure to foreign exchange risk, particularly within its SME sector, mirrors patterns observed in other emerging markets. Historically, rapid financial integration and external borrowing liberalization have introduced structural vulnerabilities when accompanied by inadequate risk management frameworks. Well-documented cases from Brazil, Indonesia, and Thailand illustrate the consequences of unchecked FX risk accumulation and the policy responses that mitigated systemic spillovers. Studies such as Eichengreen et al. (2005) on currency mismatches and emerging market crises and Goldstein and Turner (2004) on balance sheet vulnerabilities in developing economies emphasize the critical need for institutional safeguards to prevent capital flow volatility from undermining financial stability.

Brazil, during the 2010s, experienced a surge in unhedged corporate foreign debt, particularly among SMEs and state-owned enterprises, making them highly susceptible to currency depreciation. In response, the government introduced mandatory hedging regulations, requiring firms with significant FX liabilities to maintain a minimum level of hedged exposure. Empirical analyses have shown that these measures significantly reduced default rates during periods of currency turbulence, demonstrating the effectiveness of regulatory intervention in mitigating FX-related financial distress.

Following the Asian Financial Crisis, Indonesia implemented compulsory FX hedging for corporates with substantial external debt, alongside targeted subsidies to lower the cost of hedging for SMEs. This policy intervention was informed by extensive post-crisis research highlighting the dangers of currency mismatches, such as the work of Corsetti, Pesenti, and Roubini (1999). By reducing the prevalence of unhedged positions, Indonesia was able to improve corporate balance sheet resilience and minimize financial contagion risks.

Thailand’s experience following the 2013 Taper Tantrum further underscores the value of institutionalized FX risk monitoring. Recognizing that systemic exposures had built up over time, Thai regulators introduced a centralized FX risk surveillance system, enabling real-time monitoring of external liabilities across corporate balance sheets. This framework provided policymakers with early warning signals, allowing for targeted interventions during periods of heightened global financial volatility.

Policymakers: A Proactive Oversight Role

In India, the lack of granular, real-time data on FX exposures—particularly among SMEs and mid-sized firms—remains a critical blind spot. While macroeconomic indicators such as foreign exchange reserves and external debt-to-GDP ratios suggest resilience, firm-level data is limited, impeding regulators’ ability to assess emerging vulnerabilities before they escalate. Closing this information gap requires mandatory reporting frameworks that capture sector-specific FX liabilities, currency compositions, and hedging strategies. This is especially relevant for SMEs, where data collection and publication of risk indicators should be a priority.

The introduction of minimum hedging requirements for significant FX exposures could serve as a crucial policy safeguard. Drawing from Brazil and Indonesia’s experiences, such requirements could prevent an unchecked buildup of unhedged foreign liabilities, particularly among SMEs and SOEs with high leverage ratios.

Systematic stress testing and scenario analysis must also become an integral component of India’s financial stability framework. Regulators should evaluate corporate balance sheets under adverse currency movement scenarios, assessing potential solvency and liquidity risks. These exercises can provide early warning indicators, allowing policymakers to adopt targeted measures before external shocks materialize into broader financial distress.

Furthermore, a centralized FX risk management platform, led by the Reserve Bank of India, could provide SMEs with institutional support by offering hedging instruments, market intelligence, and financial advisory services. This would lower the cost and complexity of FX risk management for firms with limited treasury capabilities, encouraging greater participation in hedging markets.

Corporate India: Strengthening Internal Resilience

Corporate India must internalize the importance of comprehensive FX risk management as an essential pillar of financial resilience. A robust corporate treasury function, equipped with advanced risk assessment tools, can significantly enhance firms’ ability to navigate external volatility.

Strengthening FX governance entails:

Conclusion

India’s aspiration to attain developed-market status by 2047 will depend on its ability to effectively manage emerging macro financial vulnerabilities, particularly those linked to external financing risks. SMEs, despite being key engines of growth, are increasingly exposed to FX risk, which, if left unchecked, could evolve into a systemic fragility.

Policymakers must strengthen institutional safeguards by enhancing data transparency, implementing minimum hedging requirements, and integrating FX stress testing into regulatory oversight. Meanwhile, corporate India must adopt a proactive approach to risk management, improving treasury governance and embedding hedging strategies into financial decision-making.

By aligning financial stability imperatives with economic expansion, India can ensure that external vulnerabilities do not become a constraint on its growth ambitions, preserving the resilience of its financial system on the path to 2047.

Chart 5: Summary of Key FX Risk Trends and Policy Implications