While global innovation leaders invest 2-4.5% of their GDP in R&D, the figure stands at 0.64% for India. In this post, Mondal and Pohit contend that the country ought to recognise R&D as an economic engine, raising public investment and the contribution of the private sector. Further, instead of only playing catch-up, there is a need to proactively develop a technology forecasting strategy.

What drives true innovation – talent, ambition, or opportunity? In reality, innovation is driven by investment: consistent, strategic, and future-oriented spending on research and development (R&D). Nations that dominate the global technology landscape today – whether the United States, Japan, South Korea, or China – did not get there by chance. They got there by investing where the future is. India now stands at a similar crossroads. If we aspire to a Viksit Bharat1 by 2047, India’s sluggish response to R&D cannot be a supporting activity; it must be treated as the economic engine.

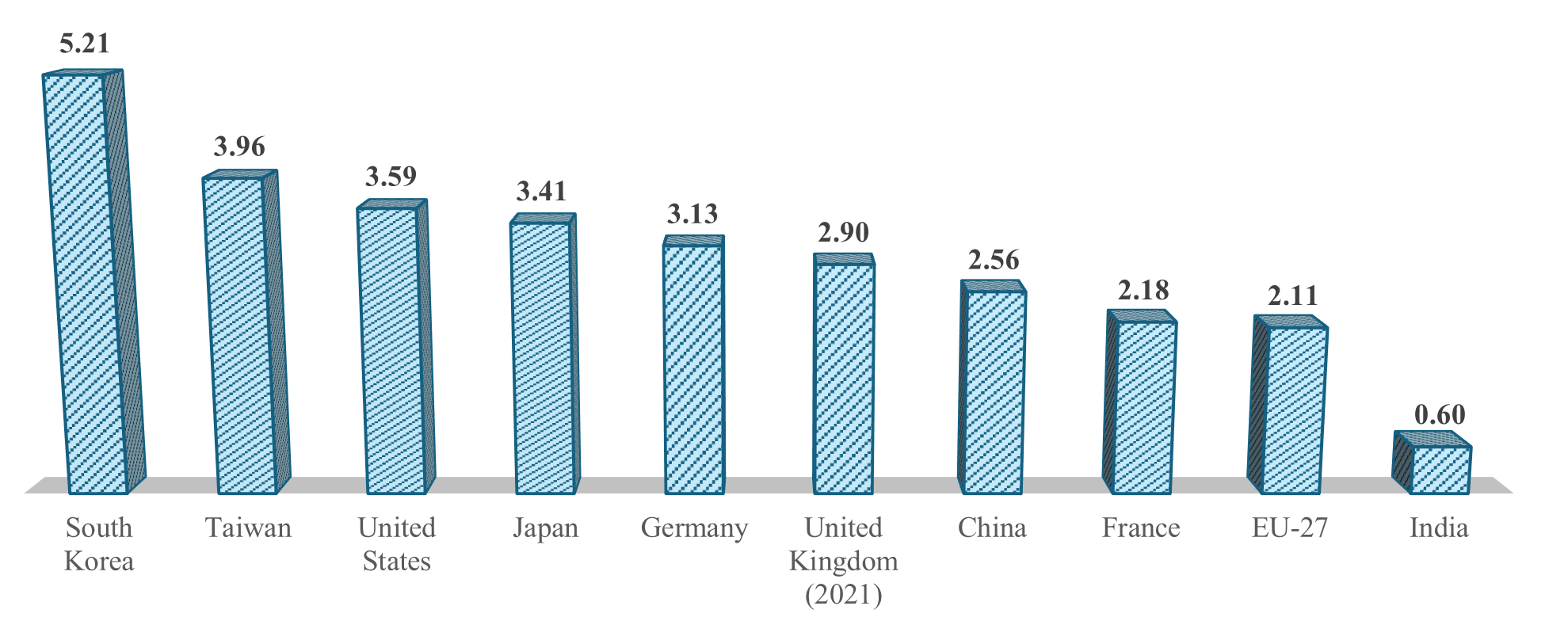

For over a decade, India has urged its industries to innovate and manufacture domestically. Yet, the country’s R&D spending tells a different story. According to the latest national R&D statistics, India’s Gross Expenditure on Research and Development (GERD) stood at 0.66% of GDP (gross domestic product) in 2018-19 and 2019-20, and then dropped marginally to 0.64% in 2020-21. In contrast, the global average is 1.8%, and innovation leaders routinely invest 2-4.5% of GDP. Even smaller East Asian economies – South Korea and Taiwan – invest between 3% and 5% of GDP annually. India’s private sector contributes only 36% to total R&D expenditure, compared to 50-70% in advanced economies.

Figure 1. GERD and GERD-to-GDP ratio, by selected region or country, 2022 or most recent year

Source: National Center for Science and Engineering Statistics, National Patterns of R&D Resources (2021-22 edition); Organisation for Economic Co-operation and Development, State of Industry R&D in India (IIFL Securities, 2024).

The result is predictable. India enters late into emerging technology arenas. By the time we master an existing technology, the market has already moved ahead – either up the value chain or into new scientific frontiers. This delays value capture, reduces competitiveness, and limits the gains Indian firms can enjoy from innovation-led growth.

What leading nations do differently

The difference between leading and lagging nations lies in one critical capability: technology foresight. While India has often reacted to global developments, others have anticipated them.

In Japan, technology forecasting exercises involve more than 2,000 top scientists and technologists, mapping out possible technology trajectories over a 25-year horizon. The outputs directly shape budget priorities, industrial strategy, and R&D funding. Japan’s early foresight in robotics and materials science ultimately enabled it to become a global leader in advanced manufacturing.

China’s transformation is even more striking. Its first major foresight initiative dates back to 1956, involving over 1,000 senior scientists who identified long-term science and technology priorities. In 2003, China conducted a major foresight exercise – “Technology Foresight toward 2020” – involving 60 leading scientists and over 320 experts across 32 subfields. Technologies were evaluated not just on scientific potential but on three economic indicators: contribution to economic growth, improvement in quality of life, and national security. Among the top priorities identified were high-efficiency solar cells, advanced biofuels, gene editing, large-scale integrated circuits, antiviral therapeutics, and advanced alloys. Today, China leads in several of those same fields.

Figure 2. Strategic chain followed by global innovation leaders

India never institutionalised this rigor. Except for a limited exercise by Technology Information, Forecasting and Assessment Council (TIFAC) in the 1990s, technology foresight never became an annual or systematic function linked to budget allocation. The result: fragmented R&D investment without a sharp national focus.

India’s turning point

India is finally recognising that innovation cannot be left to chance; it must be designed. Over the last few years, major flagship missions have been launched, demonstrating a strategic shift in the government’s approach – linking innovation, investment, and industrial capability.

The most significant push came in November 2025, when the Government of India launched the Research Development and Innovation (RDI) Scheme Fund, a landmark Rs. 1 lakh crore fund dedicated to catalysing industry-led R&D. For the first time, India’s innovation financing architecture places the private sector – not just government labs – at the centre of R&D expansion. This directly addresses India’s structural bottleneck: the low share of industry-funded research. If India wants products and technologies to reach the market, industry must lead, academia must partner, and government must enable.

Complementing this shift is the India Semiconductor Mission (ISM), launched in 2021. Backed by a Rs. 76,000 crore Production Linked Incentive (PLI) scheme – Rs. 65,000 crore of which is already committed – the mission is creating India’s semiconductor ecosystem. India has approved 10 semiconductor projects across six states, with total investments reaching Rs. 1.60 lakh crore. These include the country’s first commercial Silicon Carbide fabrication plant in Odisha. Semiconductors are the backbone of every modern technology – from smartphones to electric vehicles to national security assets. For the first time, India is not attempting to catch up; it is laying the groundwork to compete.

Similarly, the Deep Ocean Mission (DOM), launched in September 2021 with Rs. 4,077 crore, places India firmly in the global race for deep-sea resources and marine biotechnology. With 7,517 km of coastline and strategic access to deep-sea mineral reserves, India recognises that future resource security will not depend solely on land-based extraction.

Meanwhile, the IndiaAI Mission, approved in 2024 with Rs. 10,371.92 crore, aims to “Make AI in India and Make AI Work for India”. The mission has already expanded computing infrastructure from an initial target of 10,000 Graphics Processing Units (GPUs) to 38,000 GPUs, dramatically improving access for startups, researchers, and enterprises. At a time when global AI compute costs are skyrocketing, enabling public access to AI infrastructure is a competitive advantage.

Beyond missions and budgets, India’s biggest strategic edge is something intangible yet transformative: Digital Public Infrastructure (DPI). Unlike Western economies where digital rails are owned by private corporations, India has built open, interoperable platforms that democratise access to technology.

A notable example is the Unified Payments Interface (UPI). In August 2025 alone, UPI processed over 20 billion transactions worth Rs. 24.85 lakh crore, representing 85% of India’s digital payments. UPI now operates in seven countries—including France, Singapore, UAE, and Mauritius – showcasing that Indian technology can scale beyond borders. UPI proves something fundamental: innovation does not only emerge from high R&D spending; it emerges from public digital infrastructure that fuels experimentation.

DPI is enabling a unique innovation model – frugal, scalable, inclusive, and exportable. But DPI cannot compensate for underinvestment in frontier technologies like deep tech manufacturing, biotechnology, advanced materials, and semiconductors. For that, India must invest significantly more.

However, many of these sectors have been selected based on the experiences of other countries. From the Indian perspective, we need to undertake a deep-down technology forecasting exercise to narrow down the sectors where investment in R&D may give fruits in the next 20 years.

Innovation cannot be purely aspirational – it must be funded

India has the talent, the demographic dividend, and the ecosystem. What we need now is aggressive investment and prioritisation.

If India is serious about becoming a developed nation by 2047, R&D expenditure must rise to at least 2% of GDP over the next decade, with the private sector contributing 60% or more. This is not a cost – it is an investment in economic competitiveness, technological sovereignty, and national power.

Another problem with India’s innovation system is that we are largely engaged in incremental innovation and not breakthrough innovation. Nine out of 10 breakthrough innovations end up failing. In the Indian R&D system, no one wants to be associated with failure, as the committee members of the research grantee or the researchers may come under the CAG (Comptroller and Auditor General) lens for wasteful expenditure.

India’s rise will not be defined by how fast it adopts existing technologies, but by how boldly it invests in creating the next ones – the path to Viksit Bharat begins when India stops catching up and starts setting the pace with other nations in the race.

The views expressed in this post are solely those of the authors, and do not necessarily reflect those of the I4I Editorial Board.

Note:

Viksit Bharat, meaning “Developed India”, Viksit Bharat 2047 is the government’s vision to transform the country into a self-reliant and prosperous economy by 2047. Economic growth, technological upgradation, infrastructure development, social empowerment, and sustainability are the criteria of this programme.

Share this Publication

Latest Publications

Op-Eds

22 May 2026

India’s new labour reforms: Occupational Safety, Health and Working Conditions Code